The Main Principles Of Paul B Insurance

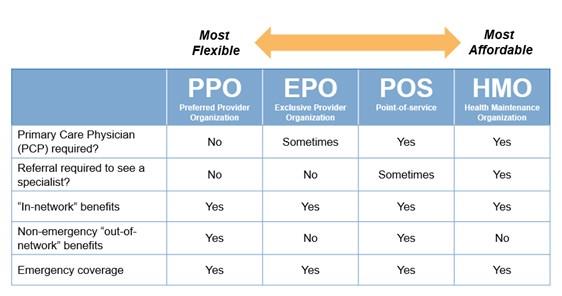

Related Topics One reason insurance concerns can be so confounding is that the medical care market is frequently altering as well as the insurance coverage intends used by insurance companies are tough to classify. Simply put, the lines in between HMOs, PPOs, POSs and various other types of protection are typically blurry. Still, understanding the make-up of numerous plan types will be practical in reviewing your choices.

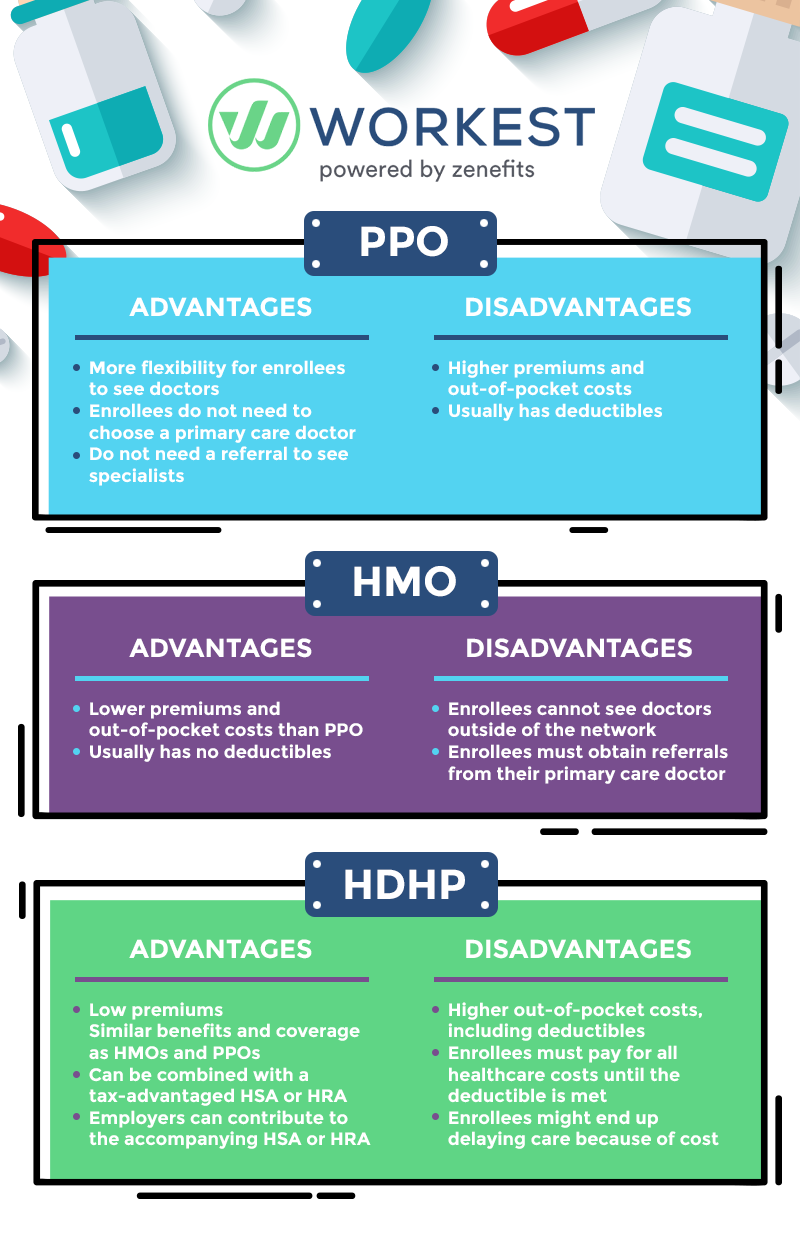

PPOs normally offer a broader selection of providers than HMOs. Costs might resemble or somewhat greater than HMOs, and out-of-pocket prices are typically higher and a lot more challenging than those for HMOs. PPOs enable participants to venture out of the company network at their discretion as well as do not need a recommendation from a health care physician.

As soon as the deductible quantity is reached, added health expenditures are covered in conformity with the provisions of the medical insurance policy. For example, a staff member may after that be accountable for 10% of the prices for care gotten from a PPO network service provider. Down payments made to an HSA are tax-free to the company and staff member, and money not spent at the end of the year might be rolled over to spend for future clinical expenses.

The Best Strategy To Use For Paul B Insurance

(Company payments have to coincide for all employees.) Employees would be in charge of the very first $5,000 in clinical costs, but they would certainly each have $3,000 in their individual HSA to spend for medical costs (and also would certainly have a lot more if they, as well, added to the HSA). If employees or their households exhaust their $3,000 HSA part, they would certainly pay the following $2,000 out of pocket, whereupon the insurance coverage plan would certainly start to pay.

(Certain limitations may put on highly compensated individuals.) An HRA must be funded entirely by a company. There is no limit on the amount of cash an employer can add to worker accounts, however, the accounts might not be funded through staff member wage deferrals under a lunchroom plan. In addition, employers are not permitted to reimburse any kind of component of the balance to employees.

Do you recognize when one of the most terrific time of the year is? No, it's not Christmas. We're speaking regarding open registration period, child! That's! The wonderful time of year when you reach contrast health and wellness insurance intends to see which one is appropriate for you! Okay, you obtained us.

The 6-Second Trick For Paul B Insurance

When it's time to pick, it's vital to recognize what each strategy covers, how much it sets you back, and where you can utilize it? This stuff can feel challenging, yet it's less complicated than it appears. We placed together some useful understanding steps to assist you really feel positive about your choices.

Emergency treatment is commonly the exception to the regulation. Pro: The Majority Of PPOs have a good selection of companies to pick from in your area.

Con: Greater premiums make PPOs much more expensive than other kinds of strategies like HMOs. A health care company is a wellness insurance plan that usually just covers treatment from doctors who help (or agreement with) that particular plan.3 So unless there's an emergency situation, your strategy will not spend for out-of-network treatment.

The Best Strategy To Use For Paul B Insurance

More like Michael Phelps. The strategies are tiered according to exactly how much they set you back and also what they cover: Bronze, Silver, Gold and also Platinum. (Okay, it's true: The Cre did have some platinum documents as well as Michael Phelps never won a platinum medal at the Olympics.) Key fact: If you're qualified for "cost-sharing reductions" under the Affordable Care Act, you must pick a Silver strategy or far better to obtain those decreases.4 It's great to understand that plans in every classification offer some sorts of totally free preventive treatment, and some offer free or reduced medical care services before you fulfill your insurance deductible.

Bronze strategies have the most affordable regular monthly costs yet the greatest out-of-pocket costs. As you function your way up with the Silver, Gold and Platinum groups, you pay much more in costs, but less in deductibles and coinsurance. Yet as we discussed in the past, the extra prices in the Silver group can be lessened if you get approved for the cost-sharing reductions.

Decreases can decrease your out-of-pocket healthcare costs a lot, so get with one of our Recommended Local Companies (ELPs) that can assist you discover what you may be qualified for. The table below shows the portion that the insurance policy company paysand what you payfor protected expenses after you meet your deductible in each strategy group.

Not known Details About Paul B Insurance

Various other prices, often called "out-of-pocket" costs, can build up promptly. Things like your deductible, your copay, your coinsurance amount as well as your out-of-pocket maximum can have a large effect on the complete price. Below are some expenditures to hug tabs on: Insurance deductible the Go Here amount you pay before your insurance policy company pays anything (with the exception of official website complimentary preventative treatment) Copay a collection amount you pay each time for things like physician brows through or various other services Coinsurance - the percentage of medical home care solutions you are in charge of paying after you've struck your insurance deductible for the year Out-of-pocket maximum the annual restriction of what you are in charge of paying by yourself One of the best ways to conserve cash on medical insurance is to use a high-deductible health strategy (HDHP), specifically if you don't expect to routinely make use of clinical services.

These work rather much like the other wellness insurance policy programs we explained currently, but technically they're not a type of insurance.

If you're attempting the DIY path and also have any kind of remaining inquiries about health and wellness insurance policy plans, the professionals are the ones to ask. And also they'll do even more than simply answer your questionsthey'll likewise find you the most effective cost! Or perhaps you would certainly like a means to incorporate obtaining fantastic healthcare protection with the chance to aid others in a time of requirement.

The 4-Minute Rule for Paul B Insurance

Our trusted companion Christian Healthcare Ministries (CHM) can help you determine your options. CHM helps households share health care expenses like medical examinations, pregnancy, hospitalization and surgery. Thousands of individuals in all 50 states have used CHM to cover their medical care requires. Plus, they're a Ramsey, Trusted partner, so you recognize they'll cover the clinical bills they're supposed to as well as honor your coverage.

Trick Inquiry 2 One of the things healthcare reform has actually done in the U.S. (under the Affordable Care Act) is to present even more standardization to insurance policy plan benefits. Before such standardization, the benefits provided diverse considerably from plan to plan. As an example, some plans covered prescriptions, others did not.